Financial planning isn’t just about retirement accounts and investment returns—it’s about making sure a surprise tax bill or existing IRS balance doesn’t knock your entire life off track. If you’re dealing with tax debt or worried you could fall behind, the right plan can turn a stressful situation into one you can actually manage.

This guide walks through practical, real‑world steps to help you stabilize your finances, tackle tax debt strategically, and protect your future—without needing to be a financial expert.

Start With A Clear Snapshot Of Your Money

Before you can fix anything, you need a clear picture of what’s going on. Many people avoid looking at their numbers because of stress or shame, but avoiding it usually makes the situation worse.

Gather your latest pay stubs, bank statements, credit card statements, loan balances, and any IRS or state tax notices. List out all income sources (even side gigs), then list your fixed expenses (rent, utilities, insurance, minimum debt payments) and variable expenses (food, subscriptions, entertainment, etc.). Include any tax debt—both the total owed and minimum monthly payments or potential installment amounts.

Seeing everything on one page helps you understand three things: how much real “wiggle room” you have each month, where you’re overspending, and how aggressively you can (or can’t) pay toward tax debt. This clarity is the foundation for any realistic plan and gives you the information you need if you decide to talk with a professional or the IRS about options.

Prioritize Cash Flow And A Basic Emergency Buffer

If tax debt is stressing you out, it’s tempting to throw every extra dollar at the IRS. But if you don’t have any cushion, the next car repair, medical bill, or missed paycheck can push you right back into crisis—often making the tax problem worse.

Start by stabilizing your cash flow. Make sure your essential bills (housing, utilities, food, transportation, basic insurance) are covered reliably each month. Then aim to build a small emergency buffer—often $500 to $1,000 to start—before making very aggressive extra debt payments. This doesn’t mean ignoring tax debt; it means giving yourself a little breathing room so one surprise doesn’t cause a chain reaction of late fees and new debt.

Think of the emergency buffer as protection for both your present and your tax plan. With a small cushion in place, you’re more likely to keep up with any IRS payment agreements, protect your credit, and avoid new high‑interest debt that can be harder to escape than the tax bill itself.

Align Your Budget With Tax Deadlines And Obligations

Tax debt often grows because people are focused only on current bills and forget that taxes are, in effect, a “future bill” that comes due every year—or every quarter if you’re self‑employed. Smart financial planning treats taxes as a non‑negotiable part of your monthly budget.

If you work for an employer, review your paycheck withholding. Use the IRS Tax Withholding Estimator to see whether you’re on track to cover your tax liability, then adjust your Form W‑4 if needed so you’re not constantly under‑withholding and ending up with a surprise balance each year. That one change can stop a recurring tax problem from snowballing.

If you’re self‑employed, freelancing, or earning side‑gig income, create a separate “tax” savings account and move a percentage of each payment into it right away—before you use the money for anything else. Build your budget around the net amount after that tax set‑aside. This approach can dramatically reduce the risk of future tax debt and makes quarterly payments far less painful.

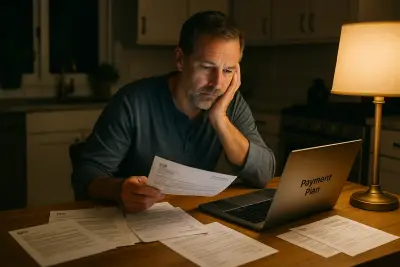

Tackle Tax Debt Strategically: 5 Actionable Tips

Many people try to “wing it” with tax debt, paying what they can when they can. A better approach is to treat IRS obligations like any other major financial commitment—with a clear, structured plan. Here are five practical, actionable tips:

- Don’t ignore IRS mail—open it and note the deadlines.

IRS notices are time‑sensitive. Ignoring them can lead to automatic penalties, liens, or levies that are much harder to undo. As soon as you receive a letter, note any deadlines and what the IRS is asking for (payment, information, a response). Put those dates on your calendar and build your plan around meeting them.

- Compare your options: full pay, payment plan, or relief programs.

List what you realistically can afford each month after essentials and a small emergency buffer. If you can’t pay in full, look into an IRS installment agreement (payment plan). For those experiencing financial hardship, options like Currently Not Collectible status or an Offer in Compromise may be available, but they require documentation and careful evaluation. Matching the right option to your situation helps you avoid over‑promising and defaulting later.

- Cut specific, targeted expenses to free up tax payment room.

Instead of vague goals like “spend less,” identify concrete cuts: pause unused subscriptions, negotiate your phone or internet bill, downgrade streaming services, or limit dining out to a specific dollar amount per month. Even $50–$150 in freed‑up cash can be redirected toward tax debt and make a meaningful difference without completely changing your lifestyle overnight.

- Prioritize high‑cost debt while staying compliant with the IRS.

Tax debt often has lower interest than credit cards but carries serious enforcement powers. The goal is usually twofold: stay compliant with the IRS (file on time, keep up with any agreement) while working down your highest‑interest debts (like credit cards). For many people, that means making required payments to the IRS, then putting any extra toward the highest‑interest balance until it’s gone—without letting tax obligations fall behind.

- Get professional help before things escalate, not after.

If you’re overwhelmed, unsure about your options, or facing liens, levies, or wage garnishments, speaking with a qualified tax professional can save time, money, and stress. They can help you review IRS notices, evaluate relief programs, negotiate payment terms, and design a plan that fits your budget. Early intervention often means more options and less damage to your finances and credit.

Protect Your Future While You Solve Today’s Problems

When tax debt feels urgent, long‑term goals like retirement or education savings can slip completely off the radar. While you may need to temporarily slow down on some goals, you don’t want to abandon your future entirely.

Once you’ve built a small emergency buffer and set a sustainable plan for your tax debt, consider at least modest contributions to high‑priority goals, especially if your employer offers a 401(k) match. Even a small contribution keeps you in the habit of saving and takes advantage of any “free money” your employer is willing to add.

At the same time, review your insurance coverage—health, auto, renters or homeowners, and, if applicable, life insurance. A tax bill is stressful, but an uncovered medical emergency or accident can be financially devastating. Proper coverage is part of a solid financial plan and protects the progress you’re making on your tax and other debts.

Finally, build simple systems that make good decisions automatic: recurring transfers to savings, calendar reminders for tax deadlines, and regular check‑ins with your budget. The goal isn’t perfection; it’s steady, realistic progress that moves you away from crisis mode and toward lasting stability.

Conclusion

Managing tax debt is ultimately a financial planning problem—not just a tax problem. When you understand your full money picture, protect your cash flow, budget for taxes like any other essential bill, and use structured strategies to deal with IRS balances, you put yourself back in control.

You don’t need to fix everything overnight. Start by getting clear on your numbers, then choose one or two steps from this guide to act on this week—whether that’s opening an IRS notice, adjusting your withholding, trimming a few expenses, or exploring a payment plan. Small, consistent moves are what turn a stressful tax situation into a manageable part of your overall financial life.

Sources

- [IRS – Tax Withholding Estimator](https://www.irs.gov/individuals/tax-withholding-estimator) – Official IRS tool to help you check and adjust your paycheck withholding

- [IRS – Paying Your Taxes: Payment Plans, Installment Agreements, and Options](https://www.irs.gov/payments) – Overview of IRS payment options, including installment agreements and other relief programs

- [Consumer Financial Protection Bureau – Getting Out of Debt](https://www.consumerfinance.gov/consumer-tools/debt-collection/getting-out-of-debt/) – Guidance on prioritizing debts, budgeting, and dealing with collectors

- [FINRA Investor Education – Emergency Funds](https://www.finra.org/investors/personal-finance/emergency-funds) – Explanation of why and how to build an emergency savings buffer

- [USA.gov – Personal Finance](https://www.usa.gov/personal-finance) – Federal resource hub on budgeting, managing debt, and handling financial challenges

Key Takeaway

The most important thing to remember from this article is that this information can change how you think about Financial Planning.